By Ernest Chan and Akshay Nautiyal

Features are inputs to supervised machine learning (ML) models. In traditional finance, they are typically called “factors”, and they are used in linear regression models to either explain or predict returns. In the former usage, the factors are contemporaneous with the target returns, while in the latter the factors must be from a prior period.

![]()

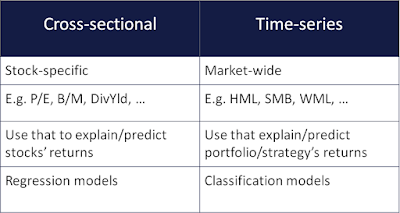

There are generally two types of factors: cross-sectional vs time-series. If you are modeling stock returns, cross-sectional factors are variables that are specific to an individual stock, such as its earnings yield, dividend yield, etc. In our previous blog post, we described how we provide 40 such factors to our subscribers for backtesting and live predictions. But as we advocate using ML for risk management and capital allocation purposes (i.e. metalabeling), not for returns predictions, you may wonder how these factors can help predict the returns of your trading strategy or portfolio. For example, if you have a long-short portfolio of tech stocks such as AAPL, GOOG, AMZN, etc., and want to predict whether the portfolio as a whole will be profitable in a certain market regime, does it really make sense to have the earnings yields of AAPL, GOOG, and AMZN as individual features?

Meanwhile, time-series factors are typically market-wide or macroeconomic variables such as the familiar Fama-French 3-factors:market (simply, the market index return), SMB (the relative return of small cap vs large cap stocks), and HML (the relative return of value vs growth stocks). These time-series factors are eminently suitable for metalabeling, because they can be used to predict your portfolio or strategy’s returns.

Given that there are many more obvious cross-sectional factors than time-series factors available, it seems a pity that we cannot use cross-sectional factors as features for metalabeling. Actually, we can – Eugene Fama and Ken French themselves showed us how. If we have a cross-sectional factor on a stock, all we need to do is to use it to rank the stocks, form a long-short portfolio using the rankings, and use the returns of this portfolio as a time-series factor. The long-short portfolio is called a hedge portfolio.

We show the process of creation of a hedge portfolio with the help of an example, starting with Sharadar’s fundamental cross-sectional factors (which we generated as shown in the blog). There are 40 cross sectional factors updated at three different frequencies – quarterly, yearly and twelve month trailing. In this exercise, however, we use only the quarterly cross-sectional factors. Given a factor like capex (capital expenditure), we consider the normalized (the normalization procedure is found in the previously cited blog post) capex of approximately 8500 stocks on particular dates from January 1st, 2010 till current date. There are 4 particular dates of interest every year – January 15th, April 15th, July 15th and October 15th. We call these the ranking dates. On each of these dates we find the percentile rank of the stock based on normalized capex. The dates are carefully chosen to capture change in the cross sectional factors of the maximum number of stocks post the quarterly filings.

Once the capex across stocks is ranked at each ranking date (4 dates) each year we obtain the stocks present in the upper quartile (i.e ranked above 75 percentile) and the stocks present in the lower quartile (i.e ranked below 25 percentile). We take a long position on the ones which showed highest normalized capex and take a short position on the ones with the lowest. Both these sets together make our long-short hedge portfolio.

Once we have the portfolio on a given ranking date we generate the daily returns of the portfolio using risk parity allocation (i.e allocate proportional to inverse volatility). The daily returns of each chosen stock are calculated for each day till the next ranking date. The portfolio weights on each day are the normalized inverse of the rolling standard deviation of returns for a two month window. These weights change on a daily basis and are multiplied to the daily returns of individual stocks to get the daily portfolio returns. If a portfolio stock is delisted in between ranking dates we simply drop the stock and not use it to calculate the portfolio returns. The daily returns generated in this process are the capex time series factors. This process is repeated for all other Sharadar cross-sectional factors.

So, voila! 40 cross-sectional factors become 40 time-series factors, and they can be used for metalabeling any portfolio or trading strategy, whether it trades stocks, futures, FX, or anything at all.

What about the opposite conversion? Can we turn time-series factors into cross-sectional factors suitable for predicting the returns of individual stocks? Actually, there is no need. You can directly add any time-series factor to your feature set for predicting individual stock’s returns. This is equivalent to building a linear factor model with an individual stock’s returns as dependent variable and the time-series factor as independent variable, a process well-known in traditional finance.

DISCLAIMER

- The information and opinions contained in this document are for background purposes only and do not purport to be full or complete. The information in this document is not personalized investment advice or an investment recommendation on the part of QTS Capital Management, LLC (“QTS”). No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document, and no liability is accepted as to the accuracy or completeness of any such information or opinions.

- All investments involve the risk of a loss of capital. QTS believes that its proprietary investment program and research and risk-management techniques moderate this risk through the careful selection of portfolio investments. However, no guarantee or representation is made that QTS’ investment program will be successful, and investment results may vary substantially over time. Past performance is not necessarily indicative of future results.